Risk Management, Asset Allocation, and Building a Balanced Investment Portfolio

>> Finance & Investing>> Risk Management, Asset Allocation, and Building a Balanced Investment Portfolio

Risk Management, Asset Allocation, and Building a Balanced Investment Portfolio

Successful investing is not only about choosing the right assets—it is about managing risk and allocating assets wisely. Many investors lose money not because their investments were bad, but because their portfolios lacked balance and protection. This article explains the core principles of risk management, asset allocation, and how to build a strong, diversified investment portfolio for long-term success.

What Is Risk in Investing?

Risk is the possibility that an investment’s actual return will differ from expected results. It includes:

-

Losing part or all of your capital

-

Experiencing high price volatility

-

Facing unexpected market downturns

-

Earning lower-than-expected returns

All investments carry some level of risk. The goal is not to eliminate risk—but to control and manage it intelligently.

Types of Investment Risk

Understanding risk helps you prepare for it. Key risk types include:

-

Market Risk: Losses due to overall market decline

-

Inflation Risk: Purchasing power eroded by rising prices

-

Interest Rate Risk: Bond prices falling when rates rise

-

Credit Risk: Borrower failing to repay

-

Liquidity Risk: Inability to sell quickly without loss

-

Currency Risk: Exchange rate fluctuations

Each asset class carries a different combination of these risks.

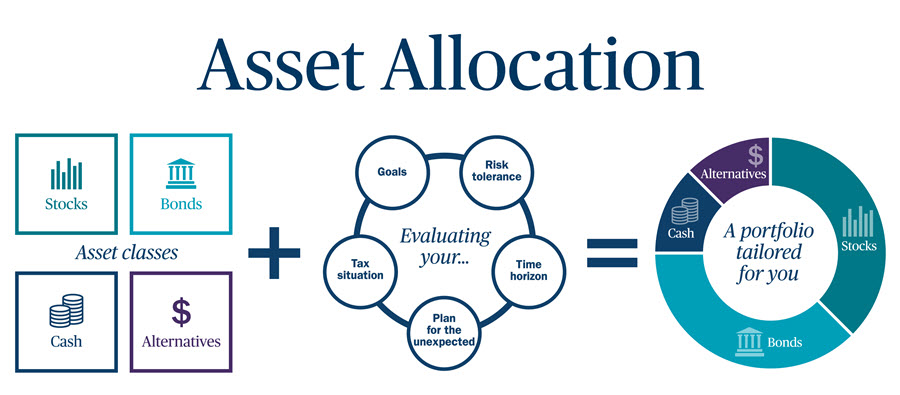

What Is Asset Allocation?

Asset allocation refers to how you divide your investment capital among different asset categories such as:

-

Stocks

-

Bonds

-

Real estate

-

Commodities

-

Cash

-

Cryptocurrencies

This decision is the most important factor in determining long-term portfolio performance—even more important than picking individual stocks.

Why Asset Allocation Matters

Proper asset allocation:

-

Reduces overall portfolio volatility

-

Protects against major losses

-

Improves long-term return stability

-

Balances growth and safety

-

Aligns with financial goals

A portfolio heavily concentrated in one asset type is exposed to greater risk if that market crashes.

Common Asset Allocation Models

Here are a few general models based on risk profiles:

1. Conservative Portfolio

-

20% Stocks

-

60% Bonds

-

10% Real Estate

-

10% Cash/Gold

Designed for retirees or risk-averse investors focusing on capital preservation.

2. Balanced Portfolio

-

50% Stocks

-

30% Bonds

-

10% Real Estate

-

10% Gold/Cash

Suitable for most long-term investors.

3. Aggressive Growth Portfolio

-

70% Stocks

-

10% Bonds

-

10% Real Estate

-

10% Crypto/Alternatives

Designed for young investors with long time horizons.

These are examples—not fixed rules. Each investor’s allocation should be personalized.

The Role of Diversification

Diversification means spreading investments across:

-

Different asset classes

-

Different industries

-

Different geographical regions

-

Different company sizes

The goal is to avoid putting all your money in one place. When one investment performs poorly, another may perform well, helping stabilize your overall returns.

What Is Portfolio Rebalancing?

Over time, some assets grow faster than others, causing your original allocation to change. Rebalancing means adjusting your portfolio periodically to maintain your desired asset mix.

For example:

-

If stocks grow from 50% to 70% of your portfolio, rebalancing would involve selling some stocks and reallocating to bonds or other assets.

Rebalancing:

-

Controls risk

-

Locks in profits

-

Maintains investment discipline

Most investors rebalance annually or semi-annually.

Risk Management Tools for Investors

Risk management involves more than diversification. Key tools include:

-

Stop-Loss Orders: Limit losses on individual positions

-

Position Sizing: Control how much you invest per asset

-

Emergency Fund: Provides cash for unexpected needs

-

Insurance: Protects against health and property risks

-

Hedging: Using gold or derivatives for protection

A well-protected investor survives market storms with less damage.

Psychological Risk and Emotional Control

One of the biggest risks in investing is not market volatility—it is human emotion. Fear leads to panic selling. Greed leads to buying at market tops. Successful investors:

-

Follow clear investment rules

-

Avoid emotional decision-making

-

Stay invested during market downturns

-

Focus on long-term goals

Emotional discipline is one of the strongest risk management tools.

Building a Balanced Portfolio: Step-by-Step

-

Define your financial goals

-

Determine your time horizon

-

Assess your risk tolerance

-

Choose your asset allocation

-

Diversify within each asset class

-

Invest consistently

-

Rebalance periodically

-

Review your portfolio annually

This structured approach removes guesswork and emotional bias.

Conclusion

Risk management and asset allocation are the backbone of long-term investment success. A balanced portfolio protects capital during market downturns while still allowing steady growth during strong markets. By diversifying wisely, rebalancing regularly, and controlling emotional behavior, investors can significantly improve both safety and performance over time.